Frequent changes in the value of your 401k can cause you to lose sleep over your retirement plan, especially if you check your account balance often. But if you understand what causes these fluctuations, you might find that there’s no reason to worry. So why does your 401K go up and down?

Your 401K may go up and down due to an aggressive portfolio and stock market volatility. They consist mainly of equities that fluctuate more because the investments are more volatile than debt/cash instruments. Stock market volatility affects the prices of 401k investments, causing fluctuations.

Read on for an in-depth discussion on the causes of the up and down movements of your 401k and what to do about them.

IMPORTANT SIDENOTE: I surveyed 1500+ traders to understand how social trading impacted their trading outcomes. The results shocked my belief system! Read my latest article: ‘Exploring Social Trading: Community, Profit, and Collaboration’ for my in-depth findings through the data collected from this survey!

Table of Contents

Reasons That Your 401k Goes Up and Down

There are two possible explanations for why your 401k account balance fluctuates:

- Your asset allocation

- Market volatility

For the sake of clarity, let’s tackle the effect these two factors have on your 401k performance separately.

Asset Allocation

Your 401k account’s performance primarily depends on your asset allocation. When your 401k goes up and down, it’s a reflection of the performance of your investments and how much of your savings are invested in each type.

You might experience varying levels of fluctuation in the value of your 401k plans due to the following:

- The types of investment vehicles and securities you opt for.

- How you optimize your asset allocation to your goals and time horizons.

That’s why it’s common for two participants working in the same company and contributing similar figures each month towards the same 401k plan to experience varying levels of volatility, return, and appreciation.

Why does asset allocation have such an impact on your 401k’s volatility?

You see, different assets carry varying levels of risk. And while the risk isn’t necessarily the same thing as volatility, the two often go in hand. Why?

Because an asset whose price fluctuates rapidly exposes you to a higher risk of bad outcomes.

Generally, debt instruments such as bonds are safer in terms than equities of risk and volatility. The trade-off is that they don’t provide as much growth potential as equities.

In fact, equities have the highest growth potential, which is why they’re often included in retirement plan investment portfolios alongside debt instruments despite their higher risk.

The more equities held in your 401k investment portfolios (whether through individual stocks or funds that invest primarily in stocks), the higher the chances of frequent fluctuations in the plan’s value.

The same applies to risk.

Market Volatility

Trends in the stock market are also bound to play a part in how much your 401k fluctuates in value, which applies even if you don’t hold company stock in your portfolio. Why? Because most mutual funds invest in a combination of debt instruments and equities to give 401k participants a chance to grow their money and mitigate risk through diversification.

How stock market volatility causes your 401k to fluctuate is pretty straightforward.

As the market moves up and down, that movement affects the unit price of the investments in your 401k investment portfolio and causes the value of your retirement plan to fluctuate with the market.

One way to track market volatility is to study the movement of market indexes.

A market index refers to a hypothetical investment portfolio that represents the performance of a specific financial market segment. Typically, the value of the index is calculated based on the unit prices of the underlying investments.

Investors use market indexes as benchmarks for market trends. The most popular indexes for stock markets include Nasdaq Composite Index, Dow Jones Industrial Average (DJIA), and S&P 500 Index.

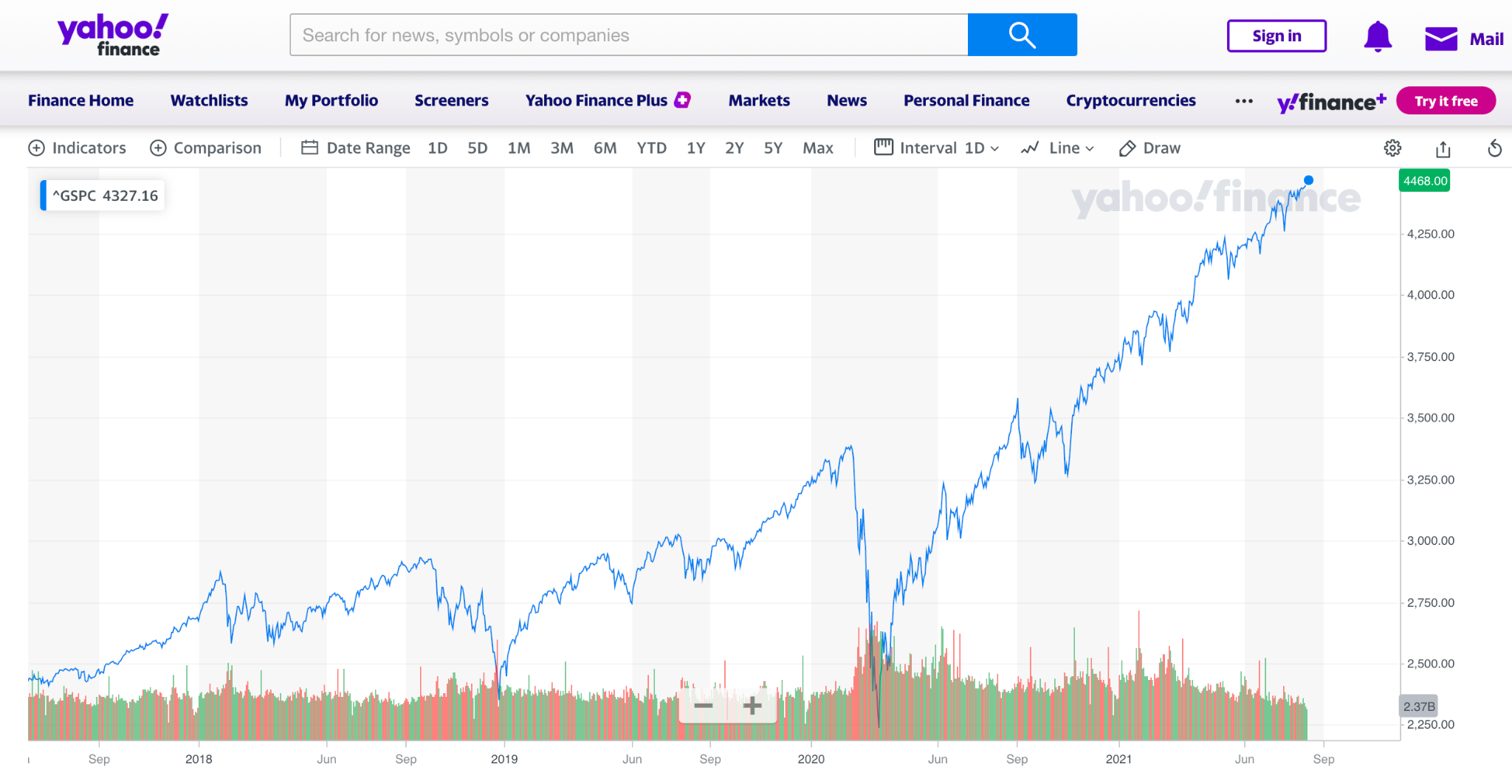

To demonstrate just how much the stock market fluctuates, let’s look at the performance of the S&P 500 Index between January 2021 and July.

A quick look at this chart from Yahoo finance shows a general upward trend in the S&P 500 Index between January and July. However, closer examination reveals that even though this market index has generally maintained an upward curve in that period, there are several up and down movements.

Since these movements affect stock prices, chances are they’re the cause of the fluctuations in the value of your 401k.

What You Can Do About Your 401k Going Up and Down?

Generally, it’s normal for your 401k to fluctuate in value over time. However, drastic changes, especially close to retirement, might warrant some attention.

There isn’t a universal right course of action to fix this kind of volatility because every 401k plan is different. With that said, it’s possible to adjust your portfolio’s risk and volatility through asset allocation.

Here’s how that works.

How to Reduce 401k Volatility?

When I talk about mitigating 401k risk and volatility through asset allocation, I’m referring to increasing the proportion of debt/cash securities in your portfolio. To clarify how this works, let’s look at three hypothetical situations.

Scenario A

In the first situation, let’s assume you invest 60% of your 401k funds in equities and the remaining 40% in debt or cash securities. As an FYI, this is the standard allocation for most 401k participants.

In this scenario, your portfolio would have moderate volatility thanks to the bond/cash securities. Meanwhile, the equities would allow you to enjoy substantial long-term growth.

Scenario B

In the second scenario, let’s assume that you get more aggressive with your portfolio allocation. You invest 70% of your 401k savings in equities and split the rest between debt and cash.

In this case, the potential for long-term growth is higher because you hold more equities in your portfolio. However, your account wouldn’t have the smoothest of rides in terms of volatility because you hold fewer debt/cash securities.

Scenario C

In the last situation, let’s assume you go on the defensive with a more conservative asset allocation. This time around, you invest 85% of your 401k in debt/cash securities and the remainder in equities.

The result of such asset allocation would be low potential long-term growth but a smooth ride in terms of volatility.

As a general rule, you should be concerned about 401k volatility and consider rebalancing your asset allocation when you’re close to retirement. If your plan fluctuates when you still have several decades to save for retirement, you can afford to wait for things to stabilize, especially if the fluctuations are due to stock market movements.

Note: As you can see, the more debt/cash securities you hold in your portfolio, the less volatile it becomes. However, this comes with the caveat of lower potential long-term growth, meaning it isn’t always the best move.

The Basics of 401k Plans

Most people know how a 401k plan works:

You commit a portion of your salary to retirement on contributions via paycheck deferrals, potentially with your employer matching your contributions up to a certain dollar amount/percentage to encourage you to save.

If you’re reading this, you’re probably familiar with this basic definition. You likely also know that your 401k doesn’t just sit idle in a bank account, but it’s invested in Exchange-Traded Funds (ETFs), mutual funds, and possibly shares of the company for which you work.

In most cases, you get to decide how much of your retirement savings are invested in each option through what’s known as asset allocation.

What many 401k participants don’t know is how their asset allocation affects the value of their 401k. It’s one of the main determinants of the performance of such retirement plans and potentially why your 401k goes up and down.

Author’s Recommendations: Top Trading and Investment Resources To Consider

Before concluding this article, I wanted to share few trading and investment resources that I have vetted, with the help of 50+ consistently profitable traders, for you. I am confident that you will greatly benefit in your trading journey by considering one or more of these resources.

- Roadmap to Becoming a Consistently Profitable Trader: I surveyed 5000+ traders (and interviewed 50+ profitable traders) to create the best possible step by step trading guide for you. Read my article: ‘7 Proven Steps To Profitable Trading’ to learn about my findings from surveying 5000+ traders, and to learn how these learnings can be leveraged to your advantage.

- Best Broker For Trading Success: I reviewed 15+ brokers and discussed my findings with 50+ consistently profitable traders. Post all that assessment, the best all round broker that our collective minds picked was M1 Finance. If you are looking to open a brokerage account, choose M1 Finance. You just cannot go wrong with it! Click Here To Sign Up for M1 Finance Today!

- Best Trading Courses You Can Take For Free (or at extremely low cost): I reviewed 30+ trading courses to recommend you the best resource, and found Trading Strategies in Emerging Markets Specialization on Coursera to beat every other course on the market. Plus, if you complete this course within 7 days, it will cost you nothing and will be absolutely free! Click Here To Sign Up Today! (If you don’t find this course valuable, you can cancel anytime within the 7 days trial period and pay nothing.)

- Best Passive Investment Platform For Exponential (Potentially) Returns: By enabling passive investments into a Bitcoin ETF, Acorns gives you the best opportunity to make exponential returns on your passive investments. Plus, Acorns is currently offering a $15 bonus for simply singing up to their platform – so that is one opportunity you don’t want to miss! (assuming you are interested in this platform). Click Here To Get $15 Bonus By Signing Up For Acorns Today! (It will take you less than 5 mins to sign up, and it is totally worth it.)

Conclusion

Ultimately, your 401k is bound to go up and down due to the aggressiveness of your portfolio and stock market trends. Rethinking your portfolio asset allocation can help stabilize things, but that often means missing potential investment growth. Thus, whether the volatility of your 401k needs addressing depends on your goals and investment time horizon.

BEFORE YOU GO: Don’t forget to check out my latest article – ‘Exploring Social Trading: Community, Profit, and Collaboration’. I surveyed 1500+ traders to identify the impact social trading can have on your trading performance, and shared all my findings in this article. No matter where you are in your trading journey today, I am confident that you will find this article helpful!

Affiliate Disclosure: We participate in several affiliate programs and may be compensated if you make a purchase using our referral link, at no additional cost to you. You can, however, trust the integrity of our recommendation. Affiliate programs exist even for products that we are not recommending. We only choose to recommend you the products that we actually believe in.

Recent Posts

Exploring Social Trading: Community, Profit, and Collaboration

Have you ever wondered about the potential of social trading? Well, that curiosity led me on a fascinating journey of surveying over 1500 traders. The aim? To understand if being part of a trading...

Ah, wine investment! A tantalizing topic that piques the curiosity of many. A complex, yet alluring world where passions and profits intertwine. But, is it a good idea? In this article, we'll uncork...